Program Highlights

(Results from October 1, 2022 through September 30, 2023)

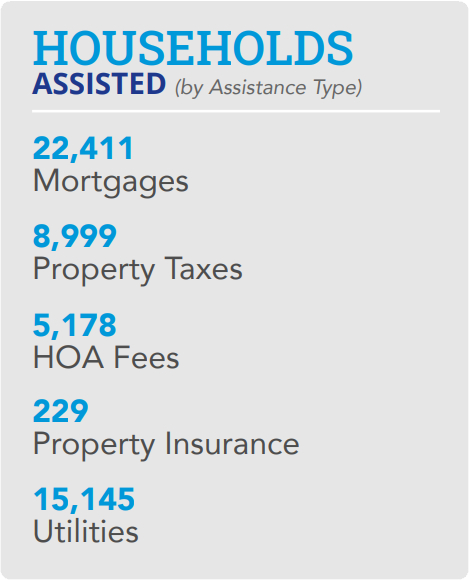

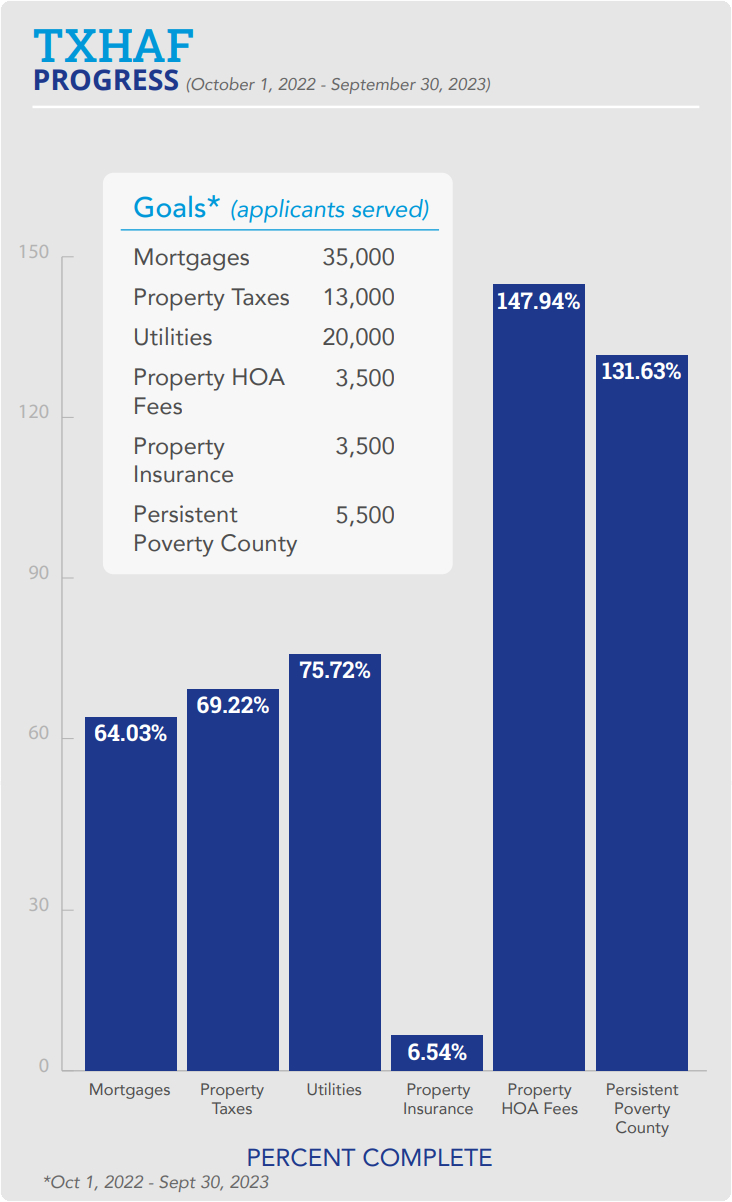

TXHAF helps low- to moderate-income homeowners eliminate past-due amounts associated with their mortgage loans, HOA fees, homeowner insurance, property taxes and/or utilities, with an emphasis on those who reside in the 52 Persistent Poverty Counties of Texas.

The most significant portion of funds are allocated to go directly to homeowners who apply for assistance. Additionally, a portion of funds supports non-profit organizations providing low-income Texans with application intake services, housing counseling and legal services.

|

|

Community Partnerships

In order to effectively reach and serve eligible homeowners throughout the state, including those in more rural areas and in areas with concentrations of non-traditional mortgage loans, TDHCA/TXHAF partnered with 32 subrecipients to provide application assistance, legal services and/or housing counseling services to program eligible homeowners.

Of the 32 subrecipients, there were 25 providing application intake services, 18 providing housing counseling and 7 providing legal services. Through 164 physical locations plus virtual and phone options, TXHAF subrecipients served all 254 counties in Texas, including the Persistent Poverty Counties.

32

Subrecipient organizations

- Coverage across all 254 Texas counties

- Operating 176 physical locations across the state

- Many locations offer virtual assistance

- Subrecipients host mobile pop-up events within local communities

- Subrecipients hosted 1,676 outreach events

Subrecipient services resulted in:

- 7,174 applications submitted

- 3,539 households assisted in Persistent Poverty Counties

- 6,732 households received housing housing counseling services

- 1,602 households received legal services

- 249 foreclosures prevented

Meeting Homeowners Where They Are